The Fed, Interest Rates and Inflation…. What may lie ahead

By Kelly Pedersen, CFP®

Whether in line to buy groceries or gas, you’ve likely experienced this first hand. The Consumer Price Index (CPI) for all items rose 0.6% for the latest January report driving up annual inflation by 7.5%. Food and energy are large contributors to the spike in inflation, and the invasion of Ukraine is likely to keep the inflation rate high for the foreseeable future.

As a result, the chances of a 0.50 percentage point Fed interest rate increase at the next FOMC meeting rose to 44.3%,, compared with 25% just before the latest data release, according to CME data. Chances of a sixth quarter-percentage point hike this year have risen to about 63%., compared with about 53% before the release.

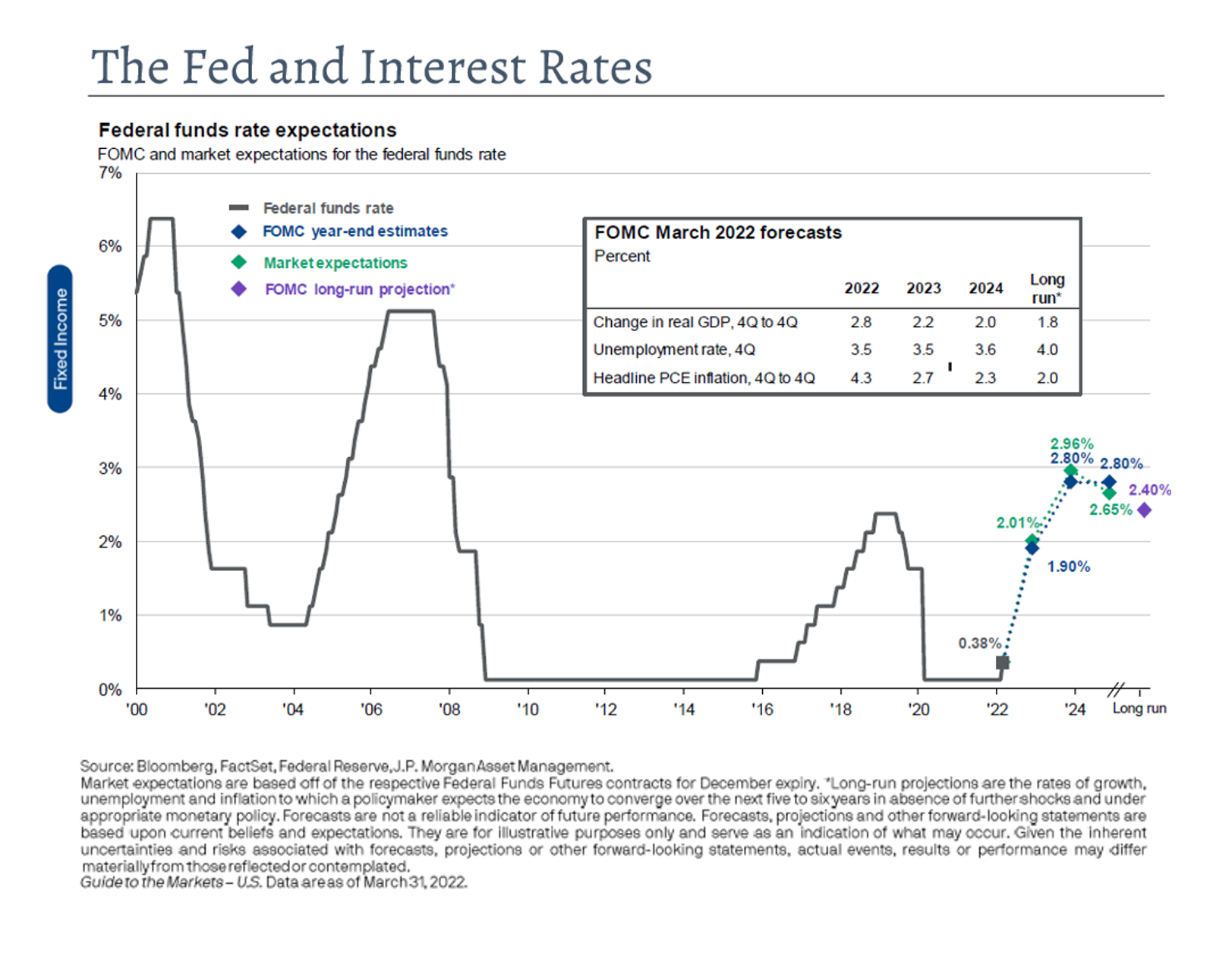

With that background, the chart below shows what the market has priced in for expected interest rate hikes compared to what the Fed has indicated it will do. For the first time in months, these expectations are right inline. It is likely by the end of 2022 we will have Fed Funds above 2% for the first time since 2019. Some believe rates will keep rising, but there is another camp that thinks rate hikes will need to taper to keep us from falling into a recession as supply chain issues correct.

While the inflation outlook previously suggested that March (data is always delayed so we still don’t have March data) could be the peak of inflation, two factors have since changed that outlook. First, the invasion of Ukraine has lead to many disruptions in the global food supply, as well as a massive hike in energy costs.. Second, China has since imposed a national lockdown in response to another strain of COVID, which will likely further exacerbate the supply chain issues the United States has with imports from China.

While the inflation outlook previously suggested that March (data is always delayed so we still don’t have March data) could be the peak of inflation, two factors have since changed that outlook. First, the invasion of Ukraine has lead to many disruptions in the global food supply, as well as a massive hike in energy costs.. Second, China has since imposed a national lockdown in response to another strain of COVID, which will likely further exacerbate the supply chain issues the United States has with imports from China.

We believe some of these economic indicators could start to turn in the near months and start to get better. However, market anxiety about potential Fed “overtightening” won’t abate until there are clearer indications that inflation is under control. Expectations are that the easing of supply shortages could help reduce inflation, but the invasion of Ukraine and the lock downs in China could derail some of the natural reversions to normalcy in the short term. The Fed will need to walk a very fine line of raising rates at the appropriate pace to try and curb inflation.

Keep in mind the markets are priced out for 12 months of forward earnings (for the most part). So long as the Fed telegraphs its hikes and the market digests that information in small doses, it should absorb the changes well. However, any unexpected shocks from the Fed could send the market reeling. We will be watching the Fed closely, as well as labor statistics, China lock downs and the Ukraine invasion. It is a very fluid market environment, and we will keep you apprised as to the potential impact, and opportunities, for your portfolio.