What is a Yield Curve and Why is Everyone Talking About It?

What is a Yield Curve and Why is Everyone Talking About It?

by Kelly Pedersen, CFP®

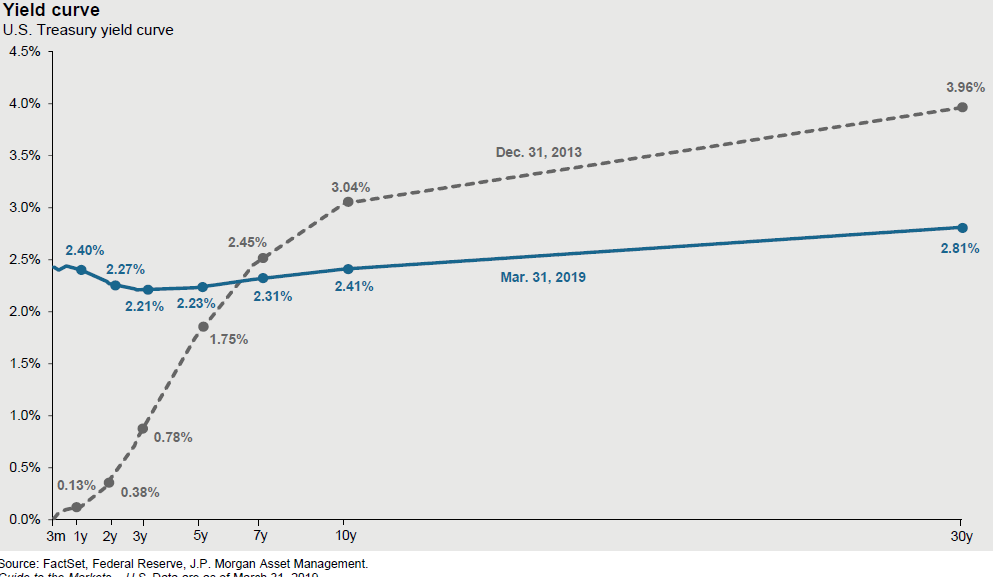

It happened, the yield curve inverted. Talking heads have made the topic go viral. Many people may be asking “What is an inverted yield curve?” In the graph below, you will find in grey a standard looking yield curve from 2013. It is just a line that plots out the rate of return for bonds of various lengths. Typically, one would expect the short-term bonds to yield less and long-term bonds to yield more, hence why yields, as plotted in a graph, tend to form a gentle “curve” the longer the bonds get.

Source: FactSet, Federal Reserve, J.P. Morgan Asset Management

Looking instead at the blue line, this is an “inverted” curve. It happens when shorter term rates are actually HIGHER than some of their longer-term counterparts and therefore when you plot them all out, the line becomes flipped over, or inverted. This is happening right now and it’s because the Fed raised interest rates four times last year. The short end of the curve increased but the longer-term bonds did not move much.

What does this mean? Well, you will hear a LOT of reporters telling you this means we will have a recession in 12-24 months. Typically the market is a leading indicator of this and will sell off before the recession starts. Right now, our markets are not flashing the red light that a recession is imminent. In fact, it’s almost contrary. Markets are actually telling us they are baking in no more rate hikes and actually a possibility of a stimulus rate CUT!

Even if we were pointing toward a recession, all indicators are pointing to a very shallow recession and nothing like the GREAT Recession. Many people have attached the 2008 Financial crisis to a recession in their own minds but the reality is, a recession is just a slowing of growth for a period of time. Sometimes it’s almost a nonevent, other times it can turn into a crisis like 2008.

Caissa Wealth Strategies is a fee based registered investment advisory firm, specializing in personal, dynamic wealth management. Based in Bloomington, Minnesota, Caissa financial planning professionals provide individualized strategies for every client. You can expect more from CAISSA, and in turn, you will get a fiercely loyal advocate on your side. For more news and information on wealth management solutions, visit Caissa Wealth.