Investment Chart of the Month: Inflation

Investment Chart of the Month: Inflation

By Kelly Pedersen, CFP®

Clients and Colleagues,

As we begin 2022, we are entering into a phase of the economy that has an abundance of change. Change is not always bad, but rather an opportunity to lean into areas of the market that will benefit from new circumstances. There are winners and losers in any environment when it comes to the stock and bond markets. As we have been on calls with our portfolio managers and economic advisors, We are sharing six slides that illustrate where we are (credit to Baird, Schwab and JP Morgan for many of these charts) and where we may be headed. Here is what CAISSA is analyzing, watching and acting on:

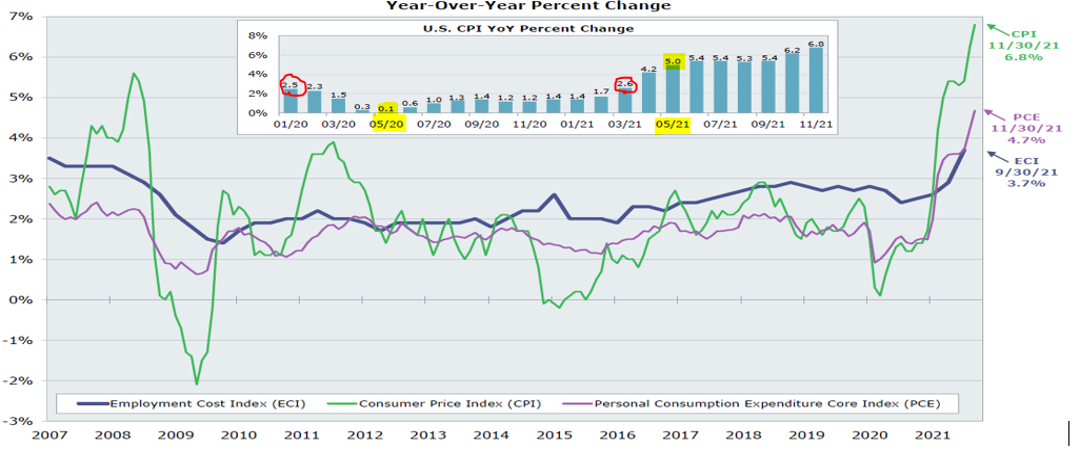

Inflation: where we were…

Inflation has overtaken headlines everywhere, and rightly so. Inflation is back: should you worry about it? We have not had inflation on goods and services like this in many years. There are different types of inflation, including some that are more “sticky,” and some that can more easily revert to normal. What we have seen from the pandemic is a disconnect between supply and demand, with demand outpacing supply. Much of that is a result of consumers spending more, as well as the hiccups in importing goods through our ports. Inflation, as reported by CPI (Consumer Price Index), has been hitting eye-opening numbers. Going into the pandemic, the Fed (Federal Reserve) had a hard time getting inflation to 2%. During the early part of the pandemic, inflation dropped to nearly nothing for several months (see below). One thing to consider is the mere equation to calculate year over year inflation growth is going to give us very abnormal numbers. If you look at the blue bar chart and the time period of May 2020 having a CPI of 0.1(remember, the goal is 2.0% and the historical average is around 3%) as you look to May of 2021, you’ll see the CPI moves to an annual increase to 5%. This sounds astounding, but when coming from a place of practically 0%, it puts it into perspective. At CAISSA, we are paying less attention to the dramatic headlines and instead looking at monthly changes. It’s likely we will need to get to March of this year before we can have any normalized numbers for inflation that aren’t skewed.

Inflation: where we are …

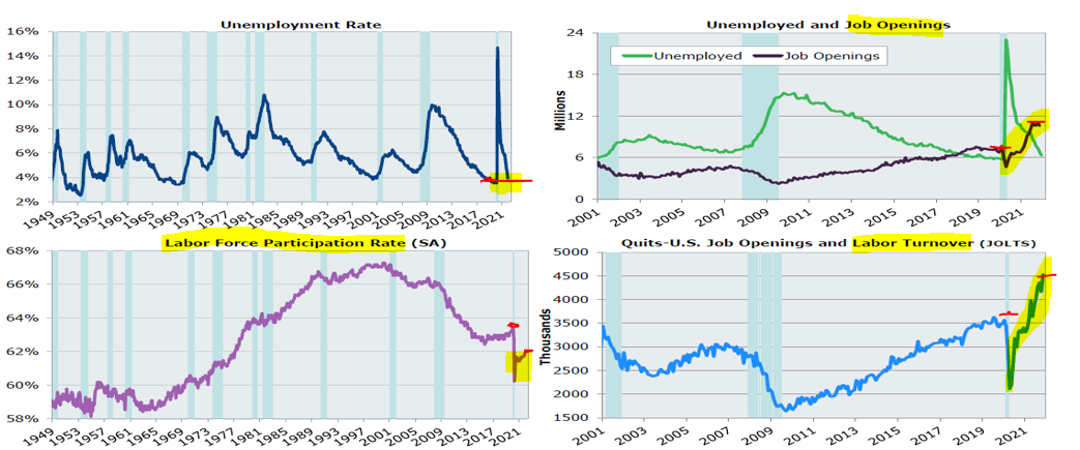

The headwind of inflation has a couple of components. For one, the pandemic has created a supply/demand dislocation. This type of inflation can be unwound as the condition normalizes. Another component is labor and wages, which is a more “sticky” type of inflation. It is very hard to reduce a person’s wages after they’ve been raised. Even though we have returned to a relatively low unemployment rate, that doesn’t tell the whole story. For all of the jobs that were lost during the pandemic, only about half of those people have come back to work (retired early, decided to stay home, created their own business). That means there are millions of people who have decided not to participate in the workforce. Hence the popular phrase “The Great Resignation.” This phenomenon makes the “war for talent” even more competitive and pushes up wages as the fight for good people rages. Once wages hike, that inflation becomes very sticky and takes a lot longer to work through the economy. CAISSA is watching this closely as a forward-market indicator for corporate earnings.

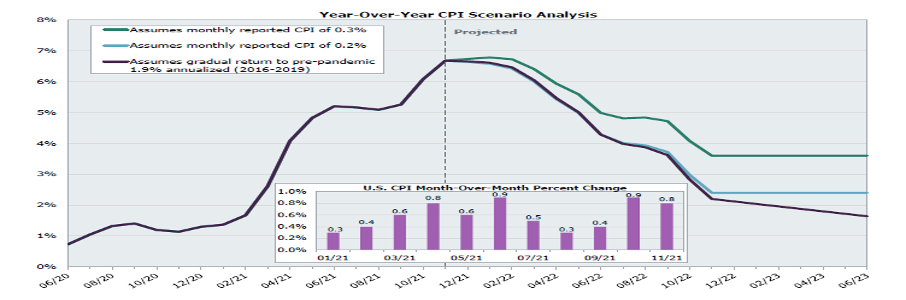

Inflation: where we are going …

If we project where we might land using monthly changes in CPI vs comparing to last year during the pandemic lows, by just normalizing the formula it is possible that we can get back to “normal” inflation in the next 12 months. How quickly it actually happens will depend on when supply chains can rectify (which they seem to be on the right path to do), and the rate at which labor participation increases (which could take much longer). Bottom line, inflation is real and it’s here but it can be understood diferrently when looking at it from another angle.

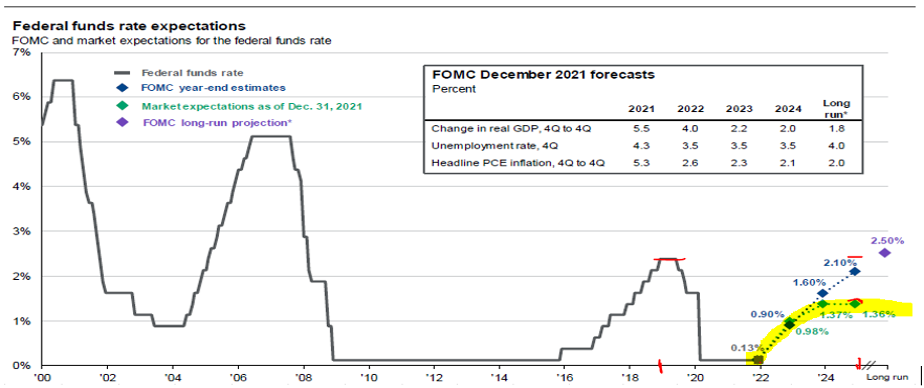

The Fed…. What to expect

Pre Covid, our Fed funds rate was about 2.4%. When the pandemic hit, the Fed pulled that back almost immediately to around 0-0.25% in order to support the economy. The Fed is now looking to normalize interest rates to counter the various economic pressures on inflation. The Fed is likely going to increase rates in March by 0.25%. The market thinks the Fed may increase another 3-4 times this year before tapering off (as indicated by the green line below). While this will affect the market by taking “easy money” off the table, it is not unreasonable to expect that the market can withstand this normalized rate without reacting negatively if we can get some other things back to pre-pandemic levels (supply issues, etc). What will likely be different is the labor market. If we don’t get participation back, then we face slower growth as well as higher wages. That could be a significant headwind for corporate profits which could cause a bad reaction in the markets.

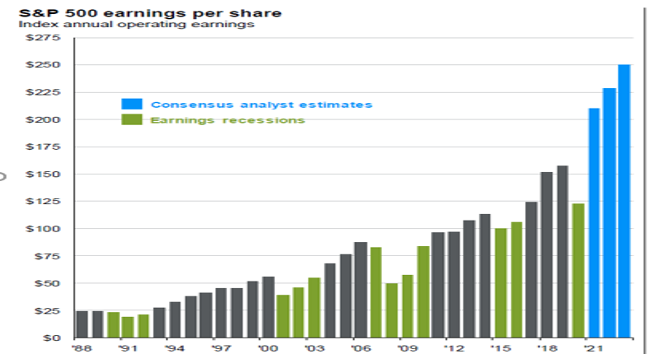

Corporate earnings…. What to expect

Markets tend to forecast a company’s future based on 12 months of earnings and then determine a price they would pay for those earnings or growth. Consensus earnings reports are indicating incremental earnings growth for 2022 on a quarterly basis, even with the supply/demand issue in full force. There is still a LOT of cash in the system that can be put to work. Additionally, the government has not spent all of the trillions of dollars allocated to support the Covid economy. Those funds will continue to be deployed over the coming years, which will be a tailwind for earnings.

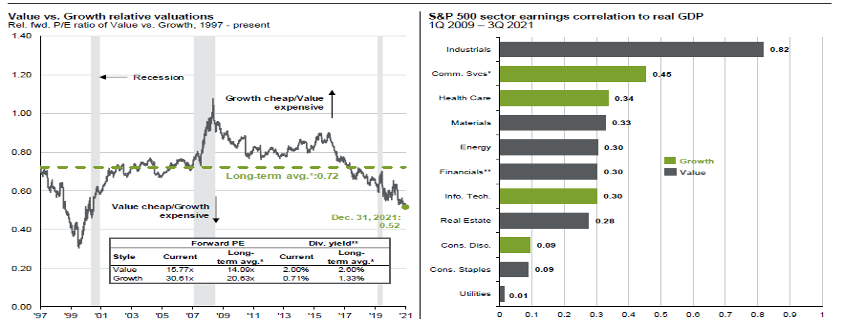

Where to lean in your portfolio

In a year when there are likely interest rate hikes, inflation and other headwinds, the typical winners are value stocks and international investments. In this environment, we are taking the double overweight of growth to value off the table (which has served us quite well in the last decade). However, CAISSA will not be overweighting value as there could be normalization in value once the Fed slows their tightening.

Markets… recent volatility

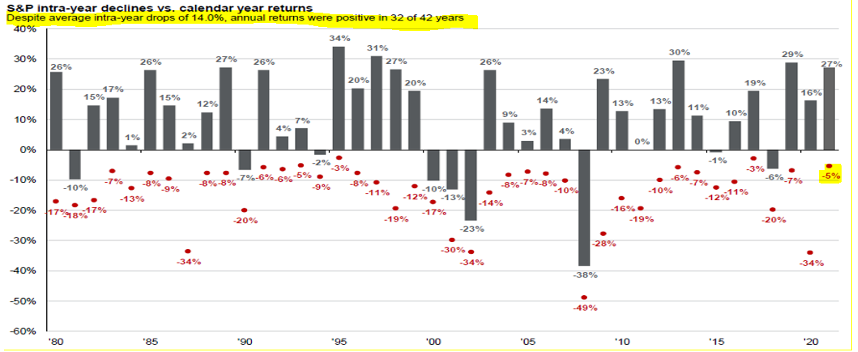

We have a different environment ahead of us than what we have been used to in the last decade of easy money and low interest rates. Raising interest rates in the face of a nationwide labor shortage will be a headwind to say the least. Portfolio managers are trying to assess what lies ahead and make adjustments. Some are panicking out of fear and some are chasing out of greed. So far in 2022, the S&P is down about 9% (depending on the day, literally). Consider this, on an annual basis for the past 40+ years we typically have seen about one -14% downturn at some point each year, every year on average. This is normal. Last year our largest intra-year pullback was about 5%. We are due. What is different this time is that it’s not just a pullback, there is a rebalancing effect between growth and value. This is also healthy. What is not healthy is to try to day trade into asset classes or sectors. CAISSA is looking at strategic moves that lean into the areas we think will provide more value in the next few years. We also subscribe to making sure we have a fully funded Tranche 1 (learn what Tranches are) (a CAISSA short term asset allocation overlay) so we can allow for the market fluctuations in Tranche 3 (the long term asset allocation).

Key takeaways for 2022

- Have an equal balance of value and growth in your domestic stock portfolio.

- Maintain your mid and small cap allocations. They are the first asset class to get beat up, and they are the first asset class to rapidly rebound from depressed economic conditions.

- Increase international exposure to full weighting (meaning not having an underweight to international stocks), including emerging markets being a very undervalued asset class.

- Add to our private equity manager to dampen volatility.

- Use our hedged equity strategy as a damper to our equity position vs pulling back our allocation to stocks.

- Toward the latter part of the year we’ll be moving from short duration fixed income into longer duration and municipals.

Inflation can be a difficult thing to understand and reign in. The Fed is comprised of very smart individuals and they still struggle exercising the best steps. CAISSA is consistently assessing the ongoing economic conditions and repositioning portfolios accordingly. If you have any questions or would like to discuss further, please call Kelly or email her at Kelly@CaissaWealth.com.